{kind=link}

[ad_1]

Editors note: This OP by Jérôme à Paris an investment banker and blogger specialising in renewable energy projects is not for the faint hearted, as it includes a discussion of the design and usefulness of contracts for difference (CfDs) designed to provide confidence to investors in a very volatile market for electricity prices.

However, the significance for the general reader is that even in the absence of consistent state policies and subsidies, solar energy is basically becoming the core part of electricity markets in many countries, such is its cost advantage over traditional carbon and nuclear based power generation.

This means the latter are frequently reduced to the status of back up supplier when the sun doesn’t shine or the wind doesn’t blow – a role they are often unsuited to due to their high fixed costs and inflexibility in responding to rapid fluctuations in the supply demand mix.

Although written by a participant in renewable energy financing, this article actually argues that the current model of guaranteed prices for renewable energy to encourage investment may need to be replaced by more flexible models which do not reward overproduction midday when the grid is already in surplus and incentivise storage solutions instead.

The solar boom is changing the game for renewable power pricing

Until recently, and despite the bitterness and polarized nature of the debate on renewables, there was actually a fairly strong alignment of interest between the general public and developers. Despite claims to the contrary, renewables did not increase costs for customers (and indeed protected them from the volatility of gas prices, in the case of fixed price regulated tariffs or equivalent CfDs), did not weaken the grid and did reduce the use, and dependency on imports, of fossil fuels. Offering renewables protection from short term price volatility made economic sense as it allowed them to attract cheaper capital and thus deliver significantly cheaper electricity.

The macro-level reality is that renewables have displaced, and reduced the revenues of, fossil fuel plants, and the subsidies that did exist in the early days were effectively paid by the incumbent generators rather than by consumers – thus their lasting hostility, and propaganda, against renewables. The rest has largely been noise.

But now, we are in a new situation, fuelled by the continued boom of solar. That trend is showing no signs of slowing down, boosted by record low prices for solar panels and increasingly by the self-interested demand from small to medium scale commercial users of electricity. It will continue unabated, even in the absence of favorable policies, as the cost advantage for these customers is increasingly the key driver for investment volumes rather than policies for utility-scale solar farms.

This is now accompanied by a boom in battery storage projects (BESS), and combinations of renewables+storage, in particular batteries+solar. This is resulting in power systems that are increasingly dominated by solar for large parts of the day and the year, bringing power prices down to zero or even below at times, as covered extensively by Julien Jomeaux’s blog.

While we expect that demand will adapt to that (see also next section), it does mean that renewables have now reached the scale where they are increasingly self-cannibalising, i.e. they are pushing prices down at the time they can produce, and potentially cutting down their own revenues rather than those of incumbents. It then matters a lot more than before if they are to bear that price risk or not.

Under fixed price regimes, they get revenue whatever the short term price is, and this has long been recognized as an unhealthy incentive – indeed this is what causes negative prices, when wind and solar production soars, with no signal to cut it down, and the market must balance through the residual producers cutting down or demand somehow increasing. CfDs were designed precisely to reduce that problem, by ensuring that renewables producers get (and act upon) some of the short term market signals that help balance the market on an ongoing basis, while still ensuring they get, over long periods, the stable revenues that are needed to finance the upfront investment. Typically, well designed CfDs do not apply when prices are negative, ensuring that excess renewable capacity is cut down (which is technically easy) before plants for which this is difficult technically need to stop.

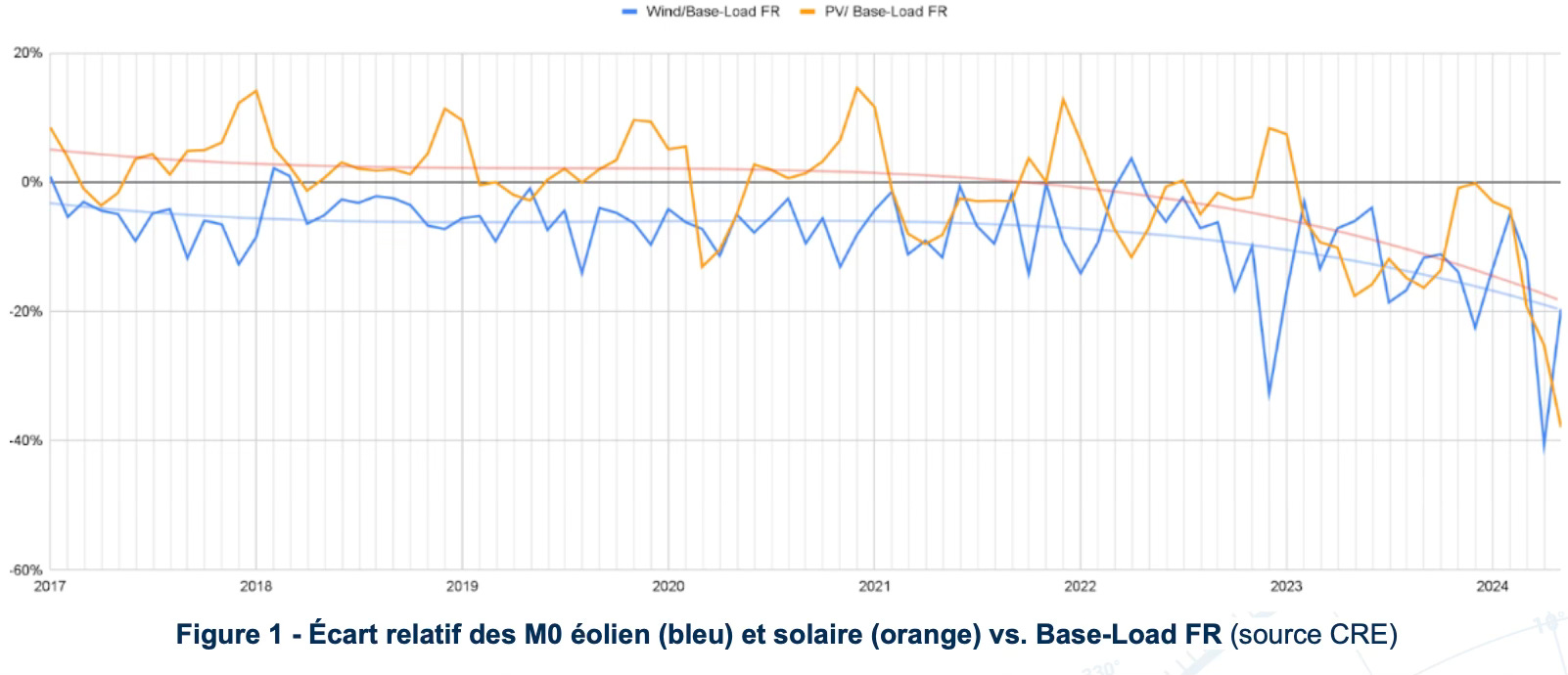

This creates a gap between the strike price of the CfD (the fixed price that procures should theoretically get) and the ‘capture price’ that they actually get, and that gap is now growing significantly. Solar, with its peak production during the day, when demand is high, actually had a capture price above the average price for a long time, but there is now so much solar that the opposite is happening – prices are collapsing when the sun is shining, and capture prices for solar are trending down.

|

Data and graph kindly provided by Xavier Laval of kilowattsol

Regulators, rightly, will not want to encourage more solar production at times when production is already plentiful (and now even excessive, at times) – and that requires that new solar producers should no longer get a positive price for their electricity when there is already too much of it – which is precisely when they will be producing… This will have an immediate impact on new investment decisions – but the scale of the problem may even require action against existing producers, which is much more problematic as they based their investment decisions (and continuing financial obligations) on the past revenue regime.

This Eurelectric presentation discusses some of the complexities of CfD regimes, beyond the mere price formula, and this ENTSO-E (association of European grid operators) report comes up with suggestions from the perspective of the grid – including, as their core proposal, to have capacity-based CfDs. Essentially, they are suggesting that wind farms or solar plants should be remunerated with a fixed yearly amount, and the grid operators would then decide when the production is actually used or not. This would definitely make projects financeable, and would help grids manage the occasional surpluses from solar, but it would certainly not incentivize developers to optimise either the location or the performance of their projects, and it would not help the development of batteries and other demand-management initiative to the same extent that current price swings will.

The ENTSO-E proposal also suggests that there may be conflicting incentives between regulators and grid as well – if the CfD payment comes from the taxpayers, the grid operators don’t really bear the cost of dumping the production from renewables, and have little incentive to improve the grids to adapt to more renewables.

Separately, there will also be an increasing tension between the logic of balancing supply and demand at the widest system level (where you only need to correct for the global net difference, which is always smaller that the sum of the local net differences) than at the local level. Projects may be incentivized by their revenue regime to include storage or other features that allow for optimisation at their specific location but this might not be optimal for the wider grid to manage.

To give a simplified example, imagine you have a zone with a surplus, and one, some distance away, but connected, with a deficit. A system-wide grid allows the surplus to balance the deficit with no change in local production. Local optimisation would push the producers in the surplus area to reduce production or store it, and would likely cause expensive marginal production (like gas-fired or diesel plants) to be started to cater for the deficit in the other area, resulting in a worse outcome overall

Market design needs to adapt to a fast changing generation fleet on an ongoing basis, taking into account the existing grid and its physical and geographical constraints, the very slow permitting process for new grid infrastructure, and the relentless growth of solar. In that context, price regimes for storage capacity is going to be one of the critical drivers of new investment (given that the solar surge is a daily phenomenon, short term storage to at least spread that generation over the evening and maybe the next morning will be a large part of the solution), and the interface between that regulatory framework and that for generation will be tricky.

We personally believe that

- renewable developers can no longer get a blank check for bringing new capacity online without regard for how their production profile fits into the system, so pricing mechanisms that give them exposure to capture price are essential. Capacity based mechanisms have too many drawbacks and will lead to development slowing down and the efficiency of projects going down. So far banks have been willing to take capture price risk where it exists, so cheap capital still exists – and will continue to exist for projects that can show they offer more value added than just weather-driven power generation, but this may not always be a given

- local / zonal pricing is a relevant solution to encourage investment in generation in the right places, and to signal where grid investments are the most critical

- in the context of zonal pricing, encouraging renewables developers to build hybrid projects (with solar+wind using the same grid connection, and added storage) make sense – but they should be avoided in price regimes that cover too broad an area, as they will encourage local regulatory arbitrage rather than relevant investment

- Storage projects should be encouraged on a standalone basis, and given the volatility of business models in a fast-changing environment, there should be some component of capacity-based remuneration to help support financing (but just like for generation, there also needs to be incentives to bring investment in the best places, and to optimise operations)

- the management of (mostly existing) hydro projects is going to become even more politically sensitive, as they represent a huge flexible capacity, which has often be discreetly “privatized” by the incumbent operators for the sole benefit of optimizing their own fleet rather than the system level needs. Admittedly in places like France the distinction is small, and the conflicts between energy system optimisation and other uses (agricultural needs and water management more generally) do not have simple answers, but as solar becomes a larger part of the system, the requirement to manage the day-time surplus (from solar) rather than the night-time surplus (from previously dominant baseload capacity) will become unavoidable.

In this, developers should not assume as naturally as before that whatever they do is “good for the planet’ and deserves full political support. As the industry matures, and begins to dominate the system, the trade offs will be more complicated, and regulators will increasingly have good reasons not to necessarily take the side of renewables developers.

Developers and the industry more generally needs to take that into account.

Jérôme à Paris is a French investment banker specialising in large scale energy projects and was a regular contributor on energy topics in the early days of Daily Kos – the main US liberal political blog – and also founded the European Tribune to focus on European issues. Nowadays he focuses on financing renewable energy projects and writes occasional blogs to counteract widespread public misunderstandings of renewable energy often propagated by oil and nuclear industry interests. Key themes include the death of baseload and the growth of microgeneration, storage, and international electricity distribution grids. But mostly, its about the political and economic interests at play.

His previous OPs published here are:

Why fans of nuclear are a problem today – not because they will succeed, but because they will fail…,

The (currently terrible) mood in renewables… is largely irrelevant

This is a guest slot to give a platform for new writers either as a one off, or a prelude to becoming part of the regular Slugger team.

Discover more from Slugger O’Toole

Subscribe to get the latest posts sent to your email.

[ad_2]

Source link